Are Payday Loan Apps safe for your financial future? Discover how early wage access impacts your mortgage eligibility and your path to real estate wealth.

Table of Contents

I was grabbing a quick coffee in Surat yesterday with a former client who finally closed on his first residential property last year. He’s a hard worker, but like many people in the real estate niche, his income can be a bit “lumpy.” One month he’s swimming in commissions, and the next, he’s waiting on a slow-closing deal. He showed me a few Payday Loan Apps on his phone and asked, “Are these early wage access tools actually safe, or am I just digging a hole for myself?”

It’s a question that hits home for many people in 2026. We’ve seen a massive surge in fintech tools promising “instant cash” with just a swipe. For a homeowner facing an unexpected roof leak or a property manager dealing with a sudden plumbing emergency, the siren song of Payday Loan Apps is hard to ignore.

However, as someone who spends my days looking at debt-to-income ratios and credit reports, I see the “hidden plumbing” of these apps. While they look sleek and modern, the underlying mechanics can sometimes feel like the high-interest storefronts we used to avoid. If you’re trying to build equity and maintain a solid credit score, you need to know if using Payday Loan Apps is a strategic move or a financial disaster waiting to happen.

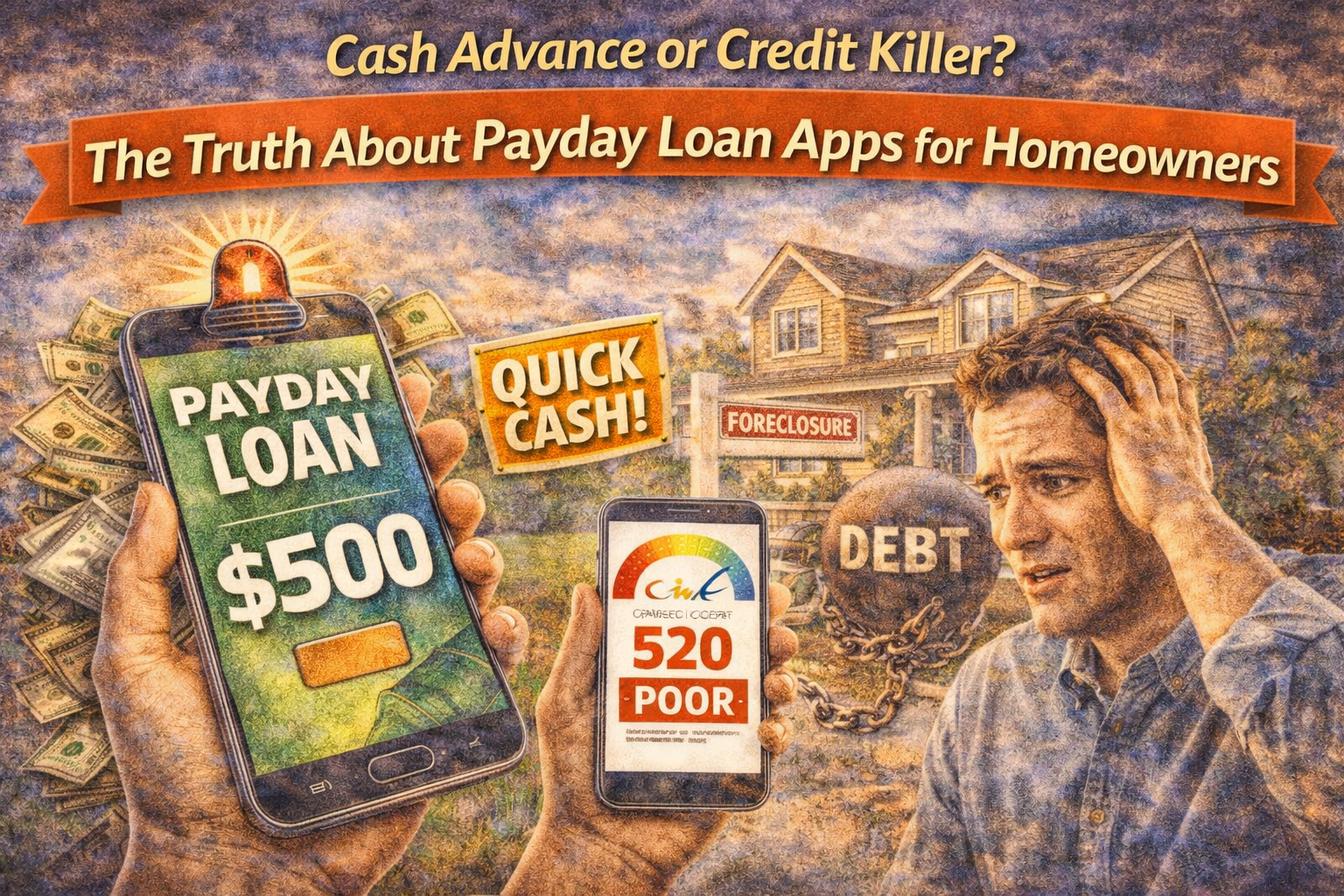

The Rise of Digital Cash Advances

In the old days, if you needed a bridge between paychecks, you had to walk into a physical office and deal with a lot of paperwork. Now, Payday Loan Apps allow you to tap into your earned wages with a few clicks. These are often branded as “Earned Wage Access” (EWA) or “Cash Advance” apps.

The primary appeal is speed. If you have a property tax bill due on Tuesday but your commission check doesn’t hit until Friday, Payday Loan Apps can fill that gap. They don’t usually perform a hard credit pull, which makes them very tempting for those with “less than perfect” credit. But speed often comes at a price that isn’t always listed as an interest rate.

Are Payday Loan Apps Actually Safe for Your Wallet?

When we talk about “safety,” we aren’t just talking about data encryption. We’re talking about your long-term financial stability. Most Payday Loan Apps claim to be interest-free, instead asking for “tips” or monthly subscription fees. If you do the math, a $5 tip on a $100 advance for one week works out to an APR of over 260%.

For a real estate investor trying to keep their overhead low, that kind of math is a nightmare. Using Payday Loan Apps too frequently can create a “cycle of dependency.” You borrow from next week’s check to pay for this week’s groceries, but then next week you’re short again. In the housing market, this lack of liquidity can prevent you from jumping on a hot investment property or handling a major repair on a rental property.

Impact on Your Mortgage Eligibility

This is the part that many buyers don’t realize until they are sitting across from a mortgage underwriter. Lenders in 2026 are increasingly looking at your bank statements, not just your credit score. If an underwriter sees a pattern of consistent withdrawals from Payday Loan Apps, it signals “financial distress.”

Even if these advances don’t show up on your credit report as a formal loan, they count toward your monthly liabilities. If you are trying to qualify for a luxury listing or a better interest rate, having Payday Loan Apps peppered through your transaction history is a red flag. It suggests that you are living paycheck-to-paycheck, which makes you a higher risk for a thirty-year commitment.

According to data often discussed by the National Association of Realtors (NAR), debt management is the single most important factor for first-time buyers. Relying on Payday Loan Apps is often the first sign that a buyer’s debt-to-income ratio is about to spin out of control.

The “Tip” Trap and Hidden Fees

One of the sneakiest things about modern Payday Loan Apps is how they gamify the borrowing process. They use friendly language like “helping a friend” or “leaving a tip” to bypass traditional lending laws.

I’ve seen clients treat Payday Loan Apps like a digital ATM, not realizing they were paying 15% in fees every single month. In the real estate business, we call this “death by a thousand cuts.” If you can’t manage your cash flow without an app, you probably aren’t ready for the unexpected costs of homeowners insurance, maintenance, and property taxes.

For a deeper look into the legal distinctions of how these apps are currently being regulated, Wikipedia’s entry on Payday Loans offers a solid foundation. Understanding the history of high-interest lending helps you spot the same old tricks inside a new, shiny app.

Better Alternatives for Homeowners and Investors

If you find yourself reaching for Payday Loan Apps every month, it’s time to look for a more sustainable “power tool” for your finances.

- The Sinking Fund: Treat your house like a business. Set aside a small percentage of every commission or paycheck into a dedicated “repair fund.”

- Credit Union PALs: Many local credit unions offer Payday Alternative Loans. These have capped interest rates and are reported to credit bureaus, actually helping you build a score.

- HELOCs: If you have built up equity in your residential property, a Home Equity Line of Credit is a much cheaper way to bridge a temporary gap than any of the Payday Loan Apps on the market.

As noted by the Consumer Financial Protection Bureau (CFPB), being an informed borrower means understanding the “total cost of capital.” If you’re using Payday Loan Apps to pay for your mortgage, you are essentially borrowing at a high rate to pay for a low-rate debt. It’s bad math, plain and simple.

How to Break the Payday Loan Apps Cycle

If you are already stuck in the loop of using Payday Loan Apps, don’t panic. The first step is to stop. It sounds simple, but it’s the hardest part. You might have one “lean” month while you adjust, but it’s better than a lifetime of interest.

Start by auditing your subscriptions and your spending in the housing market. Often, we find that people use Payday Loan Apps not because they don’t have enough money, but because their money is poorly timed. Shifting your bill due dates to align with your commission checks can often remove the need for these apps entirely.

FAQ Section

Do Payday Loan Apps report to credit bureaus? Most don’t. While this sounds good if you have bad credit, it also means that your on-time payments won’t help you build a score for a future home loan. Conversely, if you fail to repay Payday Loan Apps, they can and will sell your debt to a collection agency, which will tank your score.

What is the “APR equivalent” of a typical cash advance app? If you include the fees and “tips,” the APR for Payday Loan Apps can range from 150% to over 400%. This is significantly higher than even the most expensive credit cards on the market.

Can I use Payday Loan Apps if I am self-employed as a real estate agent? Some apps require a consistent “W-2” style direct deposit to verify income. This makes many Payday Loan Apps difficult for 1099 contractors or independent brokers to use, though some newer apps are starting to analyze bank account data instead.

Are Payday Loan Apps regulated by the government? In 2026, many states are moving to regulate these tools more strictly. However, many Payday Loan Apps currently operate in a “gray area” by claiming they aren’t technically providing loans. This is why it’s so important to read the fine print before clicking “accept.”

Will using Payday Loan Apps stop me from getting a mortgage? It won’t be an automatic rejection, but it will lead to more questions from your lender. They will want to know why you need short-term advances and if you have enough “reserve capital” to handle the responsibilities of owning a residential property.

Conclusion

At the end of the day, your home is likely your biggest asset, and your credit is your biggest leverage. Don’t let Payday Loan Apps nibble away at your financial foundation. While they offer a quick fix for a temporary problem, they often create a long-term headache that can stall your real estate goals for years.

The most successful people I know in the real estate niche aren’t the ones with the most cash; they are the ones with the best cash flow management. Ditch the Payday Loan Apps, build your emergency fund, and focus on building real equity instead of paying for digital “tips.”