Thinking of using your home equity to grow your portfolio? Learn the real risks and rewards of using a HELOC to Buy an Investment Property before you sign.

Table of Contents

I was sitting in a bustling café in Surat last month, catching up with an old client who had just celebrated ten years in his family home. Over the years, he’s watched the local residential property market climb steadily. Between his mortgage payments and the area’s natural appreciation, he’s now sitting on a literal mountain of equity. “I want to start a rental portfolio,” he told me, leaning in. “My banker suggested using a HELOC to Buy an Investment Property. It sounds easy, but is it too risky?”

It’s a question that defines the “ambitious homeowner” phase of real estate. You’ve worked hard to build value in your primary residence, and now you want that value to work for you. In 2026, where traditional financing can feel a bit sluggish, the Home Equity Line of Credit (HELOC) has become the go-to “power tool” for aspiring landlords.

However, like any power tool, if you don’t know how to handle it, you can do some serious damage to your financial foundation. Using a HELOC to Buy an Investment Property isn’t just a simple transaction; it’s a strategic pivot that ties your family’s roof to the success of a business venture. Let’s break down the mechanics, the perks, and the very real dangers of this strategy.

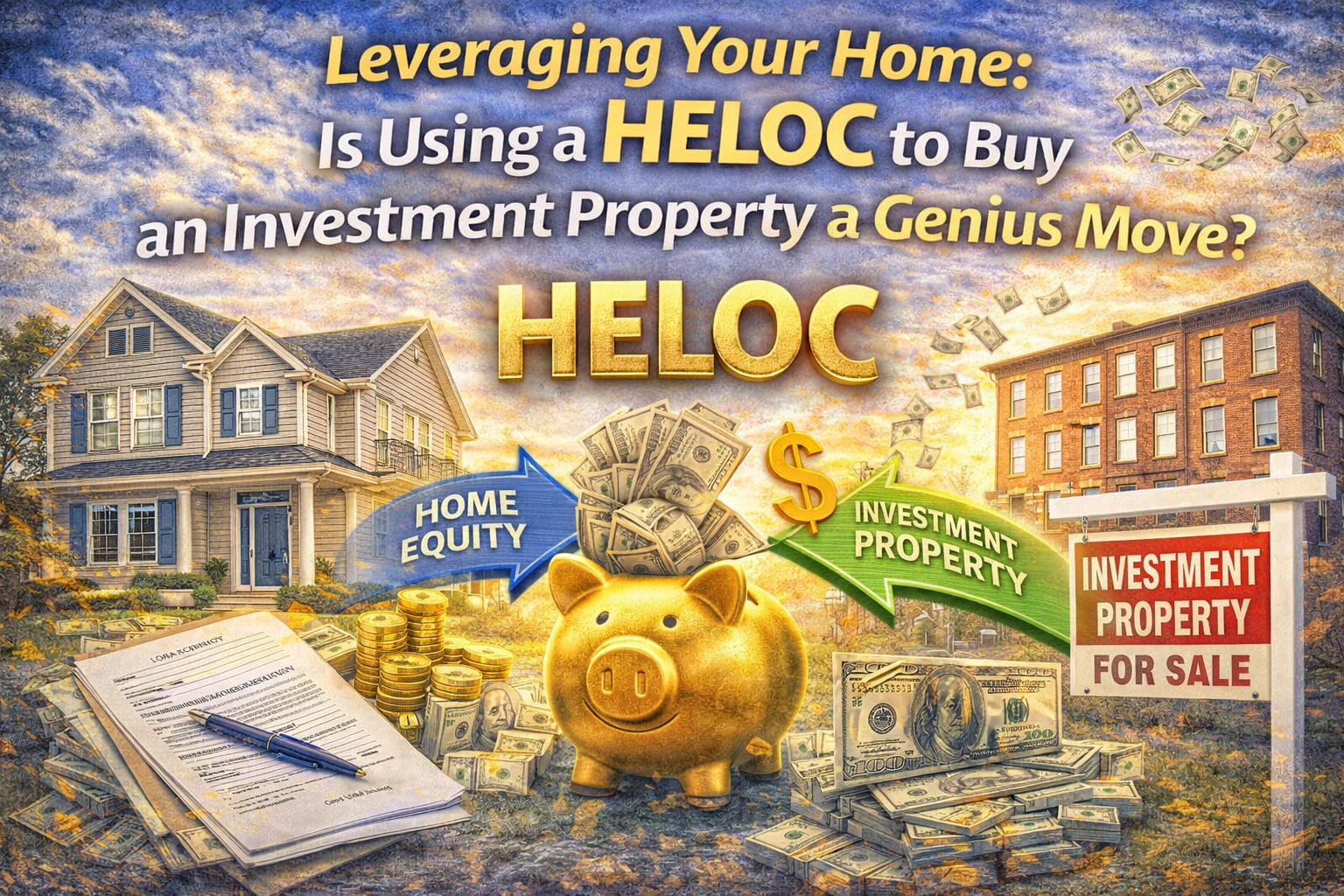

What Does It Mean to Use a HELOC to Buy an Investment Property?

A HELOC is essentially a revolving door for your home equity. Think of it like a high-limit credit card, but instead of being backed by your signature, it’s backed by your house. You get a “draw period” where you can take out cash as needed and only pay interest on what you use.

When you decide on using a HELOC to Buy an Investment Property, you are essentially pulling out the cash needed for a down payment—or even the full purchase price—of a second home. This allows you to bypass the long wait of saving up a massive cash reserve. You can move quickly when a hot listing hits the market, giving you a massive competitive advantage over other buyers who are still waiting on traditional loan approvals.

The Rewards: Why Investors Love This Move

The most obvious benefit of using a HELOC to Buy an Investment Property is the speed and liquidity. In a competitive housing market, cash is king. If you can show up to a closing table with “cash” (sourced from your HELOC), you can often negotiate a better price or a faster closing.

1. Interest-Only Flexibilty

During the initial draw period, many HELOCs offer interest-only payments. This is a massive boost to your monthly cash flow. If you use a HELOC to Buy an Investment Property that needs a few months of renovations before it’s ready for a tenant, your carrying costs stay low while you’re adding value to the property.

2. Tax Deductibility Potential

In many jurisdictions, if the funds from the loan are used strictly for investment purposes, the interest might be tax-deductible. While tax laws in 2026 are complex, using a HELOC to Buy an Investment Property can often be more tax-efficient than other forms of personal debt. Always consult with a tax professional to ensure you’re documenting the “tracing” of those funds correctly.

3. Lower Interest Rates Than Commercial Loans

Traditional investment property loans usually carry interest rates that are 0.5% to 1% higher than primary mortgage rates. However, because a HELOC is secured by your primary residence, the interest rate is often significantly lower. Using a HELOC to Buy an Investment Property effectively lets you “borrow” your home’s lower-risk profile to fund a higher-risk venture.

The Risks: The “Double-Edge” of Equity

I have to be the bearer of some heavy news here: when you use a HELOC to Buy an Investment Property, you are putting your own home on the line. If the rental market takes a dive or you hit a long period of vacancy, and you can’t make the HELOC payments, the bank can foreclose on the house you live in.

Variable Interest Rate Volatility

Most HELOCs have variable interest rates. As we move through 2026, we’ve seen that central banks can be unpredictable. If you use a HELOC to Buy an Investment Property and interest rates spike two percent in a year, your monthly payment could balloon, eating up all your rental profit and then some. This “payment shock” is the primary reason many investors eventually refinance their HELOC into a fixed-rate product.

Over-Leveraging Your Life

If the real estate market drops, you could find yourself “underwater” on both properties. Using a HELOC to Buy an Investment Property means you are 100% leveraged. You have no “skin in the game” if you didn’t use any of your own savings. If property values drop by 10%, your net worth takes a double hit. According to data often discussed by the National Association of Realtors (NAR), over-leveraging was a key factor in previous market corrections.

Real-Life Example: The Duplex Strategy

I worked with an investor recently who used a HELOC to Buy an Investment Property—specifically a duplex in a high-demand student area. He used ₹30 Lakhs from his home equity for the 25% down payment and secured a traditional mortgage for the rest.

The rental income from the duplex covered both the new mortgage and the interest on the HELOC, with about ₹15,000 left over every month. By using a HELOC to Buy an Investment Property, he was able to acquire a ₹1.2 Crore asset without spending a single rupee of his “emergency” savings. He essentially manufactured a new income stream out of thin air.

For a deeper dive into the historical risks of secondary financing, Wikipedia’s entry on Home Equity Lines of Credit offers a great overview of how these products have evolved to include more consumer protections in recent years.

How to Do It Safely: The 2026 Playbook

If you’re dead-set on using a HELOC to Buy an Investment Property, you need a safety net. Don’t use the full amount of your available credit. I always suggest leaving at least 20% of your line of credit untouched for emergencies.

Furthermore, ensure the property management is professional. A vacant unit is a disaster when you have a HELOC payment due. When using a HELOC to Buy an Investment Property, your “break-even” point is higher because you have an extra debt to service. You need a property with strong “debt service coverage” to ensure you aren’t subsidizing the investment out of your own paycheck every month.

As noted by the Consumer Financial Protection Bureau (CFPB), being an informed borrower means understanding that the “draw period” eventually ends. When it does, your HELOC to Buy an Investment Property will enter the “repayment period,” and your monthly bill will jump significantly as you start paying back the principal. You must have an exit strategy—like refinancing the investment property—before that happens.

FAQ Section

Can I use a HELOC to Buy an Investment Property if I still have a mortgage? Yes. A HELOC is a “second lien.” As long as you have enough equity (usually 15-20% must remain in the home after the loan), most lenders will allow you to take out a HELOC to Buy an Investment Property even if you have an existing primary mortgage.

Is it better to use a HELOC or a Cash-Out Refinance? A HELOC is often better if you only need the money for a short time or if your current primary mortgage has a very low interest rate that you don’t want to lose. However, a cash-out refinance provides a fixed interest rate, which is safer if you plan on holding the HELOC to Buy an Investment Property debt for many years.

What is the “Draw Period” for most HELOCs? Typically, the draw period lasts 5 to 10 years. During this time, you can pull funds to use a HELOC to Buy an Investment Property and usually make interest-only payments. After this period, you can no longer take out money, and you must begin paying back both principal and interest.

Will using a HELOC to Buy an Investment Property hurt my credit score? Initially, your score might take a small dip due to the hard inquiry and the increase in your total debt. However, as you make on-time payments and the rental income stabilizes your finances, using a HELOC to Buy an Investment Property can actually improve your credit profile by diversifying your mix of accounts.

Can I get a HELOC on the investment property itself? It is much harder. Most lenders only offer HELOCs on primary residences. While “Investment HELOCs” do exist, they come with much higher interest rates and stricter requirements than using a HELOC to Buy an Investment Property sourced from your own home.

Conclusion

Building a real estate empire is a marathon, and using a HELOC to Buy an Investment Property can be the high-octane fuel that gets you through the first few miles. It’s an incredible tool for unlocking the “hidden wealth” inside your walls to create a more secure future.

But remember: leverage is a two-way street. Be disciplined with your numbers, over-estimate your expenses, and always protect your primary residence. If you treat your home equity with the respect it deserves, using a HELOC to Buy an Investment Property can be the smartest financial move you ever make.